Low checking balance anxiety often begins long before anything actually goes wrong. A steady paycheck may be scheduled. Bills may already be accounted for. Savings might even sit safely in another account. Yet the moment someone opens their banking app and sees a smaller checking number than expected, something shifts emotionally. The chest tightens. Routine purchases suddenly feel heavy. Groceries feel like overspending instead of necessity. This reaction is not about irresponsibility or poor planning. It is about perception, visibility, and how the brain interprets short-term scarcity signals.

Many financially stable Americans experience low checking balance anxiety in quiet, private moments. They hesitate before filling the gas tank. They delay small household purchases. They mentally replay recent spending even when the math works out. The stress appears before any overdraft, before any missed bill, and before any real financial problem. That timing makes the experience confusing and sometimes even embarrassing. If income is steady and bills are covered, why does it still feel unsafe?

The answer is not discipline failure. It is timing and emotional signaling. When the visible margin between your checking balance and zero shrinks, your nervous system interprets vulnerability. That signal can override logic. Low checking balance anxiety does not require financial instability to exist. It only requires a perceived gap between what you see and what feels safe.

If your balance drops and your body reacts before your mind does, you are not failing. You are responding to visibility and timing, not to actual collapse.

By the end of this article, you will understand why low checking balance anxiety happens, how cash-flow timing intensifies it, what research says about liquidity stress, and how a small buffer restores daily calm.

Why Logic and Income Alone Don’t Fix the Feeling

It seems logical that steady income should eliminate stress. However, income is periodic while expenses are continuous. Rent, utilities, subscriptions, groceries, and fuel leave the account at different points throughout the month. When the balance drops before the next paycheck arrives, logic does not always override emotion. This is why someone earning enough annually can still experience low checking balance anxiety in the middle of a financially stable month.

Income measures long-term sustainability. Checking balances reflect short-term liquidity. The brain reacts more strongly to short-term signals. According to the Federal Reserve’s Report on the Economic Well-Being of U.S. Households, many Americans report financial stress even when they are current on bills. Liquidity visibility, not just total income, strongly influences emotional strain. That insight explains why low checking balance anxiety persists even in households that are technically stable.

U.S. Money Insight

Research from the American Psychological Association consistently shows that money remains one of the top stressors in the United States. Much of that stress stems from short-term uncertainty and visible cash-flow gaps rather than overall earnings.

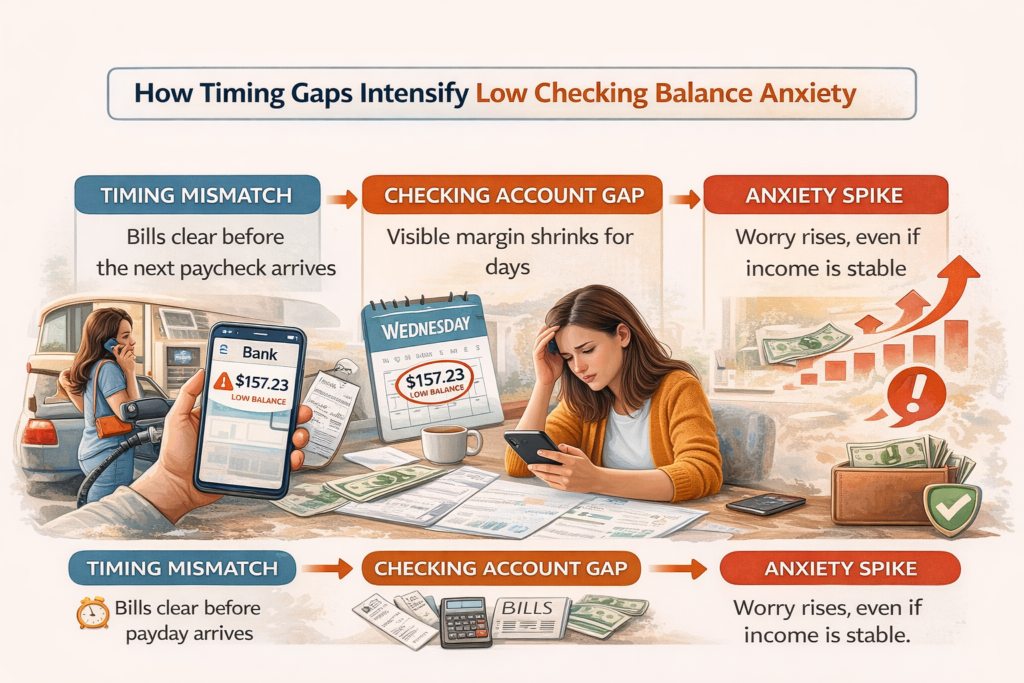

How Timing Gaps Intensify Low Checking Balance Anxiety

Low checking balance anxiety frequently spikes in the days between large bills clearing and the next paycheck arriving. This timing gap creates the illusion of scarcity. Even if savings exist elsewhere, a thin checking margin generates psychological exposure. The brain responds to what is immediately accessible, not to funds sitting in a retirement account or high-yield savings strategy.

This pattern mirrors what many readers recognize in Why Money Stress Peaks in the Middle of the Week?. Midweek often represents the lowest liquidity point in the cycle. Bills have posted. Income feels distant. Without visible margin, low checking balance anxiety can intensify even when the overall budget remains intact.

Cash-Flow Timing Insight

Liquidity research consistently shows that households experience peak stress during balance dips, not income declines. Timing mismatches amplify emotional reactions long before financial damage occurs.

Why Traditional Budgeting Misses the Emotional Layer

Traditional monthly budgets focus on totals and categories. They show whether income exceeds expenses across a 30-day period. However, low checking balance anxiety does not operate on monthly math. It operates on visible daily margin. A person can be completely within budget and still feel financially fragile if the checking balance appears thin.

This is why systems like Weekly Money Check That Finally Makes Money Feel Manageable help restore calm. Frequent visibility reduces uncertainty windows. Low checking balance anxiety decreases when reassurance arrives weekly instead of waiting for the next paycheck.

How a Buffer Changes Perception and Behavior

A small checking account cushion widens the visible gap between your balance and zero. Even a few hundred dollars can dramatically soften low checking balance anxiety. The buffer does not increase annual income. It increases emotional safety. When margin exists, routine spending feels routine again. Gas, groceries, and subscriptions no longer feel like threats.

This dynamic is explained further in How a Powerful Checking Account Cushion Changes Daily Spending Decisions. The cushion reduces overdraft risk, but more importantly, it reduces reactivity. Spending decisions become steadier. Emotional spikes decrease.

The Avoidance Loop That Keeps Stress Alive

Low checking balance anxiety often creates avoidance. Some people stop checking their accounts because they fear confirming bad news. Others check obsessively, looking for reassurance that never fully lands. Both behaviors maintain tension. Avoidance increases uncertainty, and obsessive checking reinforces hypervigilance.

This loop is similar to patterns discussed in Why Skipping Your Weekly Money Check Makes Money Feel Scarier Than It Is?. Breaking the cycle requires consistent visibility paired with margin. When reassurance becomes predictable, low checking balance anxiety begins to fade.

Consider Jason, who earns a steady income and saves regularly. Yet whenever his checking balance drops below a personal comfort number, he feels tense and delays purchases. After intentionally maintaining a modest cushion and reviewing his account weekly, he notices a shift. The same expenses occur. The same income arrives. But low checking balance anxiety no longer controls his mood. The visible margin changed the experience.

Weekly Reassurance Versus Monthly Projection

Monthly planning ensures sustainability. Weekly reassurance ensures emotional steadiness. Low checking balance anxiety responds more to predictable reassurance than to distant projections. A short weekly review combined with a consistent buffer closes the uncertainty gap faster than waiting for payday to restore calm.

For readers who want structure without overwhelm, the Daily Life Financial Planner – Complete Financial Management Bundle offers a simple weekly money check template and buffer planning pages designed to support visibility without pressure. The goal is clarity, not control.

Frequently Asked Questions

Why do I feel broke even when I’m not?

Low checking balance anxiety can make stable finances feel fragile. The emotional response often stems from timing gaps and low visible margin rather than true income insufficiency.

Is this a budgeting failure?

Not necessarily. Many people experiencing low checking balance anxiety are technically within budget. The issue is short-term liquidity perception, not long-term math.

How large should a cushion be?

The right buffer depends on your bill timing and comfort level. The purpose is to widen visible margin enough to reduce low checking balance anxiety and prevent overdraft stress.

- Notice when your stress spikes relative to payday timing.

- Observe how your behavior changes when visible margin shrinks.

- Consider how a small cushion could soften low checking balance anxiety.

Final Thoughts

Low checking balance anxiety is not evidence that you are bad with money. It is a response to visible margin and timing gaps. When you widen that margin and build steady reassurance, the emotional weight decreases. Income stability matters, but emotional safety often depends on what you can see today in your checking account.

Pingback: 7 Powerful Truths About Checking Account Balance Psychology