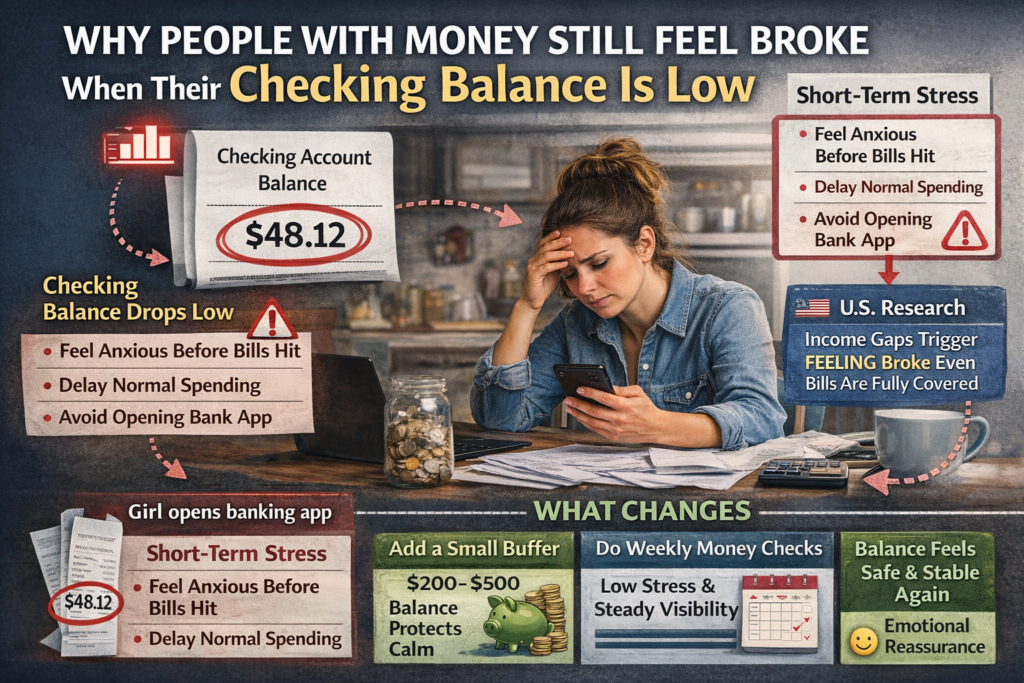

Low checking balance anxiety often begins before anything has actually gone wrong. Someone can have steady income, stable employment, and enough to cover their bills, yet still feel a wave of stress the moment their checking account dips lower than usual. The feeling is not dramatic. It is subtle and heavy. A quiet tightening in the chest. A mental replay of upcoming expenses. A sudden urge to delay even small purchases. The math may still work, but emotionally it feels like something is off.

Many everyday Americans experience this reaction in silence. They might have savings set aside, retirement contributions on track, and income scheduled to arrive in a few days. Still, when their visible balance shrinks, their mood shifts. They hesitate at the grocery store. They rethink filling up the gas tank. They postpone ordinary spending decisions because the number on the screen feels unsafe. Low checking balance anxiety shows up before overdrafts, before missed payments, and before any real financial damage occurs.

This reaction is not about discipline or intelligence. It is not a budgeting failure or proof of irresponsibility. It is about emotional safety. When visible margin disappears, the nervous system interprets the situation as risk. The checking account is where daily life happens. When that number looks fragile, it can make someone with stable finances feel temporarily broke.

If you have ever felt tense seeing a smaller balance even while knowing your paycheck is coming, you are not alone. That reaction reflects how the brain processes visibility and safety, not a personal flaw.

By the end of this article, you will understand why people with steady income can still feel broke when their checking balance is low, how timing gaps amplify that feeling, and how small structural changes reduce stress without stricter budgeting.

Why logic and income alone don’t fix the feeling

On paper, income should solve the problem. If bills are covered and savings exist, there should be no reason to feel anxious. Yet low checking balance anxiety ignores spreadsheets and projections. The brain does not evaluate annual salary or future deposits first. It evaluates what is visible right now. When the available balance shrinks, it signals reduced margin, even if only temporarily.

This is why someone earning comfortably can still feel unsettled mid-cycle. Expenses cluster. Automatic payments clear. Groceries and fuel are purchased. The visible balance dips before the next paycheck arrives. Even if the numbers are technically fine, the present-moment snapshot feels tight. The emotional reaction happens faster than logical reassurance.

This dynamic connects closely to how bills before payday create anxiety even when income is enough, where timing gaps—not totals—drive stress. The brain reacts to short-term exposure, not long-term stability.

U.S. Money Insight

Research from the Federal Reserve shows many Americans experience short-term cash-flow strain even when annual income appears stable. Timing mismatches between income and expenses increase stress more than overall earnings alone.

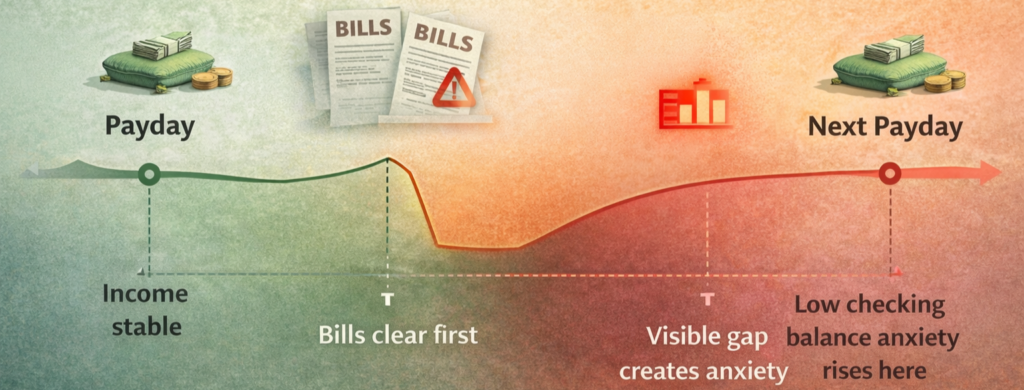

How timing gaps intensify low checking balance anxiety

Low checking balance anxiety becomes stronger during the days between expenses clearing and income arriving. This is especially common midweek, when early bills have posted and payday still feels distant. The balance reflects recent outflow but not upcoming inflow. That visual imbalance creates emotional discomfort.

This pattern is explored in why money stress peaks in the middle of the week. The week has a rhythm. Monday and Tuesday may include payments. Wednesday can feel exposed. Friday restores reassurance. The emotional dip is predictable, yet still powerful.

Without visible margin, the mind fills gaps with worst-case assumptions. Even routine expenses start to feel risky. Low checking balance anxiety grows not because the situation is catastrophic, but because the timeline feels uncertain.

Cash-Flow Timing Insight

U.S. Census data shows many households experience uneven income and expense timing throughout the month, reinforcing the emotional impact of short-term dips in available balances.

Why traditional budgeting often misses the emotional layer

Traditional budgets track categories and totals. They confirm whether spending aligns with plans. However, low checking balance anxiety does not respond to category reports. It responds to visible breathing room. A budget might say everything is on track, yet the checking account still feels thin.

This disconnect explains why many people resonate with budgeting between paychecks, which focuses on timing rather than restriction. Emotional steadiness requires protecting the lowest point in the cycle, not just managing the monthly average.

When the lowest visible number feels too close to zero, confidence drops. Even if savings exist elsewhere, the checking account is the account tied to daily life. That is where groceries, subscriptions, and fuel transactions appear. That visibility shapes perception.

How Low Checking Balance Anxiety Shapes Daily Behavior

Low checking balance anxiety influences daily spending decisions in subtle ways. People hesitate before small purchases. They delay routine spending. They open their banking app repeatedly, hoping the number feels safer. Low checking balance anxiety turns normal transactions into emotional events.

Over time, low checking balance anxiety can create patterns of avoidance. Instead of calmly reviewing money, people stop looking altogether. Ironically, this avoidance strengthens low checking balance anxiety because uncertainty grows in silence.

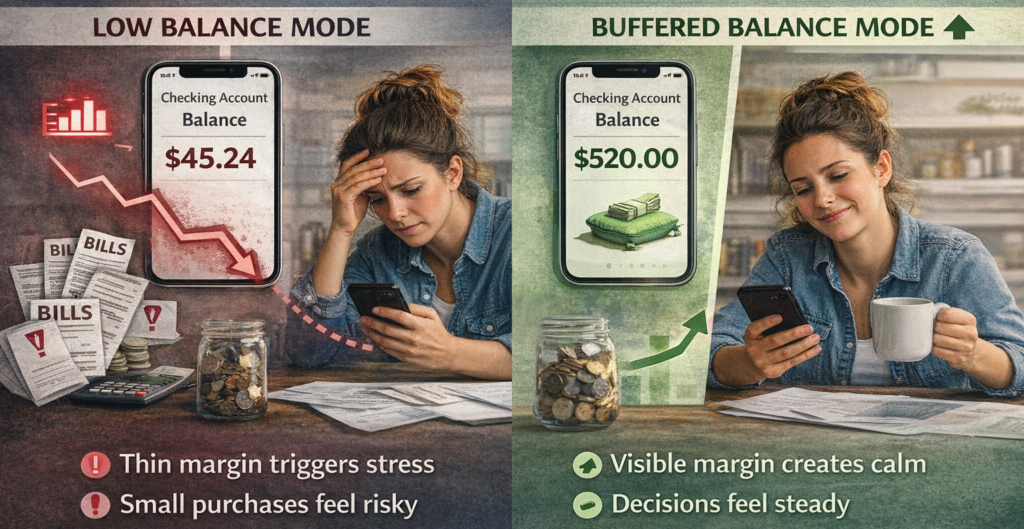

How buffers change perception and behavior

One of the most effective ways to reduce low checking balance anxiety is maintaining a modest cushion. A small, intentional buffer keeps the balance from dipping into panic territory. It does not need to be large. It only needs to create visible space between the account and zero.

This idea is expanded in how a powerful checking account cushion changes daily spending decisions. The cushion changes perception first. Perception then influences behavior. When the balance looks stable, everyday spending feels routine instead of risky.

Even a few hundred dollars can prevent emotional overreaction during tight weeks. The buffer protects the lowest point of the cycle and reduces the chance of overdraft stress, reinforcing trust in the system.

The avoidance loop that keeps stress alive

When the balance looks low, many people avoid checking it. They delay opening their banking app, hoping the discomfort will fade. Unfortunately, avoidance increases uncertainty. The mind imagines the situation is worse than it is. Low checking balance anxiety grows stronger in the absence of information.

This pattern mirrors what happens when people skip visibility practices, as explained in why skipping your weekly money check makes money feel scarier than it is. Avoidance feels protective in the moment but amplifies stress over time.

Gentle, consistent visibility reduces fear. Seeing accurate numbers—rather than guessing—calms the nervous system. Even if the balance is not ideal, clarity restores a sense of control.

A short real-life example

Imagine someone with steady income and an emergency fund in savings. Midweek, after rent and utilities clear, their checking account dips lower than usual. They begin to feel uneasy and postpone small purchases. When payday arrives two days later, the balance recovers and relief returns. Nothing catastrophic happened. The stress was driven by temporary visibility, not long-term instability.

Weekly reassurance versus monthly projection

Monthly projections answer big-picture questions, but low checking balance anxiety lives in the present moment. Weekly visibility practices shorten the window of uncertainty. They provide reassurance before imagination escalates fear.

Practices like a weekly money check that finally makes money feel manageable create structured awareness. Awareness combined with a buffer builds emotional steadiness. Income remains the same, yet confidence increases.

A supportive tool for building consistency

Staying consistent with visibility and buffer planning can feel overwhelming during busy weeks. The Daily Life Financial Planner – Complete Financial Management Bundle offers a calm structure for tracking balances, timing, and weekly clarity without turning money into a daily stressor.

Frequently Asked Questions

Why do I feel broke even when I am not?

Feeling broke often reflects low visible margin rather than actual financial instability. The checking account is a daily-life account, so its balance strongly influences emotional safety.

Is this a budgeting problem?

Usually not. It is often a timing and visibility issue. Income may be sufficient, but short-term dips create temporary stress.

How large should a cushion be?

Even a modest buffer that protects the lowest point in your cycle can reduce low checking balance anxiety significantly.

Quick Reflection

- You feel tense when your checking balance dips midweek

- You hesitate on small purchases despite stable income

- You avoid checking during low points

- You want daily spending to feel calmer

Why Reducing Low Checking Balance Anxiety Matters

Reducing low checking balance anxiety is not about increasing income overnight. It is about restoring visible safety. When low checking balance anxiety decreases, daily life feels steadier. Decisions become less reactive. Spending becomes less emotional.

The goal is not perfection. The goal is reducing low checking balance anxiety enough that money stops feeling like a constant threat. Small structural changes, like a cushion or weekly visibility, gradually weaken low checking balance anxiety over time.

Final Thoughts

Low checking balance anxiety does not mean you are irresponsible or bad with money. It means visible margin matters deeply to your sense of safety. When timing gaps are buffered and visibility improves, the feeling of being broke fades—even when income stays the same.