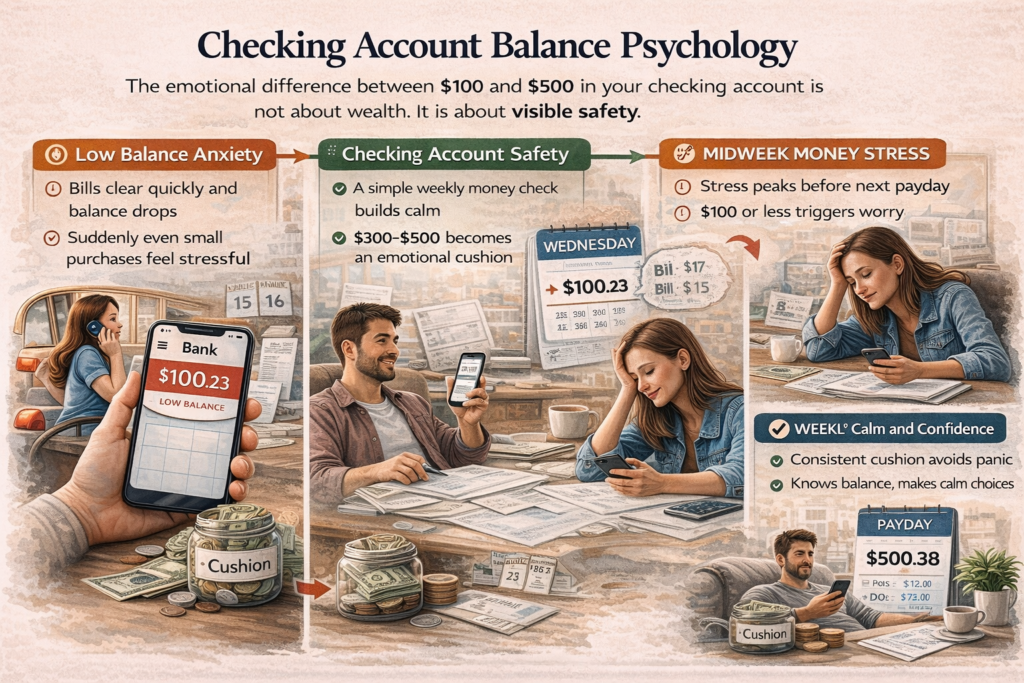

You open your banking app on a Wednesday afternoon. Nothing is late. No bill has bounced. But your balance says $100, and your stomach tightens. You start calculating gas, groceries, and the next automatic payment. Now picture the same week with $500 in your checking account. Same bills. Same income. But your shoulders relax. The math barely changed. The feeling did.

This is checking account balance psychology. The psychological difference between $100 and $500 in your checking account is not about being rich or poor. It is about visible safety. When your checking balance looks thin, your brain moves into protection mode. It reacts before logic has time to explain that payday is coming.

Most people think this stress means they are bad at budgeting. It does not. It means your brain is wired to look for margin. When the number in your checking account drops low, everyday spending feels risky. A normal grocery trip feels heavier. That emotional shift is checking account balance psychology in real time.

If your confidence changes with your checking balance, you are not weak. You are responding to visible margin. Checking account balance psychology is about emotional safety, not financial intelligence.

By the end of this article, you will understand why $500 feels calmer than $100 and how to create that steady feeling through small weekly systems.

Why Income Alone Does Not Fix This

It is common to assume that higher income removes stress. But checking account balance psychology shows that visible cash flow matters more than total earnings. You can earn steady income and still feel anxious when your checking account dips too low.

This emotional pattern connects closely with Why People With Money Still Feel Broke When Their Checking Balance Is Low. Income is long term math. Your checking balance is short term visibility. The brain reacts to what it sees today.

U.S. Money Insight

According to the NerdWallet Savings Report, 57% of Americans have less than $1,000 in savings. That means many households operate with thin financial cushions. When your checking balance drops low, your brain recognizes that margin is limited and reacts quickly.

Cash-Flow Timing Insight

Data from the U.S. Census Bureau shows that median household income can fluctuate year to year while essential expenses remain steady. When fixed costs stay high but balances move up and down between paydays, checking account balance psychology intensifies.

The Timing Gap and Visible Margin

The psychological difference between $100 and $500 in your checking account often appears right after bills clear. Rent posts. Insurance posts. Subscriptions clear. Your account drops sharply. Even if the next paycheck is already scheduled, the visible number feels exposed.

This is similar to what we explored in The Hidden Stress of Living Between Paychecks That Budgets Ignore. The gap between deposits and expenses creates emotional pressure. Checking account balance psychology reacts to the dip, not the upcoming deposit.

When Stress Feels Strongest

Stress often peaks midweek. Weekend spending hits first. Gas, groceries, and small purchases add up. That is why Why Money Stress Peaks in the Middle of the Week explains that visible balances matter more than monthly totals. The balance is lowest before it rises again.

At $100, every swipe feels like risk. At $500, everyday spending feels manageable. The numbers are not wildly different, but checking account balance psychology interprets margin as protection.

Why Traditional Budgeting Misses the Emotional Layer

Traditional budgeting focuses on categories and monthly plans. That helps with organization. But it does not always create reassurance. If your budget says you are fine but your checking account feels thin, your body reacts to the thin number.

This is why Budgeting Between Paychecks emphasizes weekly visibility. Checking account balance psychology improves when you focus on short term rhythm, not just long term totals.

Buffers, Visibility, and Reassurance

A modest cushion can shift your entire emotional response. Even an extra few hundred dollars sitting in your checking account creates breathing room. As discussed in How a Powerful Checking Account Cushion Changes Daily Spending Decisions, small buffers influence behavior and confidence.

Checking account balance psychology changes when your balance stays above your personal comfort line. That line might be $300. It might be $700. The key is consistency and awareness.

The Avoidance Loop

When balances drop, many people avoid checking their accounts. Avoidance feels easier than seeing a low number. But as explained in Why Skipping Your Weekly Money Check Makes Money Feel Scarier Than It Is, guessing increases anxiety.

Checking account balance psychology softens when you look at your balance regularly and calmly. Familiarity reduces fear.

David earns consistent income and pays bills automatically. But when his checking account drops near $120, he feels tense buying groceries. After building a $600 cushion and reviewing his balance weekly, his spending habits barely changed. His emotional state did. Checking account balance psychology shifted because the visible margin increased.

Weekly Reassurance vs Monthly Planning

Monthly planning provides structure. Weekly reassurance provides calm. When you check your balance weekly and understand what is coming next, the gap between $100 and $500 feels less dramatic. You begin to trust your rhythm.

If staying consistent feels difficult when life gets busy, the Daily Life Financial Planner – Complete Financial Management Bundle can help. It is a tool that helps people stay consistent when life gets busy and maintain weekly visibility over their checking account.

Frequently Asked Questions

Is $500 the ideal number?

There is no universal number. The right balance is the one that gives you emotional stability and breathing room.

Does this replace an emergency fund?

No. Checking account balance psychology relates to short term comfort. Emergency funds are long term protection.

Why does $100 feel stressful?

Because your brain sees limited margin. When margin feels small, alert mode activates quickly.

Quick Reflection

- What checking balance makes you feel calm?

- When during the month does stress appear?

- How would a small cushion change your weekly confidence?

Final Thoughts

The psychological difference between $100 and $500 in your checking account is about visible safety. Checking account balance psychology explains why small increases in margin create large emotional relief. With steady weekly awareness and a modest cushion, your money can feel predictable instead of threatening.

Pingback: 7 Ways Checking Account Anxiety Makes Spending Worse

Pingback: 7 Reasons Paycheck Timing Stress Matters More Than Income

Pingback: 7 Ways to Fix the Weekly Money Check Mistake