Overdraft fees often show up on a normal weekday. You are rushing out the door. You grab coffee. You stop for groceries after work. Everything feels fine.

You open your banking app later that night. The balance is lower than expected. Your chest feels a little tight.

I see this come up often when people are managing money while life keeps moving.

This post explains overdraft fees in a calm, simple way. No complicated systems. No constant checking.

What Overdraft Fees Really Are

Overdraft fees happen when you spend more money than your checking account has.

The bank still allows the payment to go through.

After that, the bank charges you a fee.

This usually comes from everyday spending.

Groceries.

Gas.

Rent.

Subscriptions.

The problem is not careless spending.

The problem is timing.

Money comes in on certain days.

Money goes out on other days.

When those days do not match, overdraft fees appear.

This happens to careful people.

This happens to organized people.

This is not about being bad with money.

Why It Matters in Real Life

Overdraft fees usually hit when money already feels tight.

You think there is enough for groceries.

A bill clears earlier than expected.

Your balance drops below zero.

Now one small purchase costs much more.

NerdWallet reports the average overdraft fee at large U.S. banks is about $35 per transaction. That is the cost of several meals for many households. NerdWallet overdraft fee data

The Federal Reserve reports that about 37 percent of U.S. adults would struggle to cover a $400 emergency. That means many people do not have extra money sitting in checking accounts. Federal Reserve household finances report

This is common.

This is not a discipline problem.

This is real life.

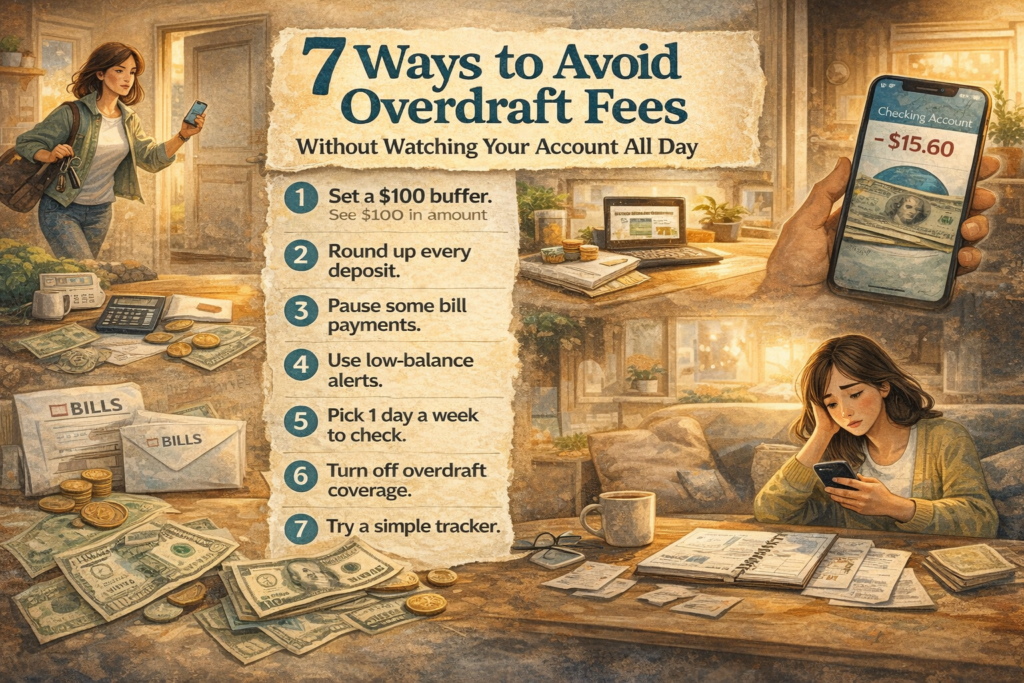

How to Handle It Simply

The simplest way to avoid overdraft fees is to keep a checking account buffer.

A buffer is a small amount of money you do not plan to spend.

It stays in the checking account.

It creates a floor your balance never goes below.

Start small.

$100 is enough to begin.

When your next paycheck arrives, leave $100 untouched.

Do not move it.

Do not spend it.

From that point on, treat your balance as if that $100 does not exist.

If your app shows $500, act like you have $400.

This buffer quietly absorbs early bills and late charges.

No daily math.

No tracking every purchase.

Just one rule.

What Happens If It Is Ignored

Without a buffer, every transaction feels risky.

You check your balance often.

You still get surprised.

Fees stack.

Investopedia explains that banks may charge multiple overdraft fees in one day if several payments clear while the account is negative. One low-balance day can trigger several fees. Investopedia overdraft explanation

This does not cause one big problem.

It causes slow stress.

Month after month.

How the Small Action Leads to the Result

The buffer works because it creates margin.

If one overdraft fee costs about $35, avoiding three saves over $100.

That is groceries.

That is gas.

That is peace of mind.

The buffer does not make you rich.

It makes your checking account calmer.

Calm reduces mistakes.

Fewer mistakes mean fewer fees.

This small buffer works because it protects you from overdraft fees without requiring constant balance checking.

Personal Notes That Matter

I see this work best for people who are tired of worrying about their balance.

This is common.

You are not bad with money.

Consistency matters more than perfection.

If the buffer gets used, rebuild it slowly.

No shame.

Ending Thought

Overdraft fees are not a personal failure.

They are a system issue.

A small buffer changes the system.

If you want help staying consistent when life gets busy, Daily Life Financial Planner – Complete Financial Management Bundle is a tool that helps people stay consistent when life gets busy.

You can also read this related guide: checking account buffer that helps you avoid overdrafts.

You are not behind.

You are building a system that fits real life.